best rates, it’s our thing

we got you

hidden fees

virtually yours

Apple Pay &

Google Pay™ on the go

can’t get safer than this

felt sweeter

you said it first

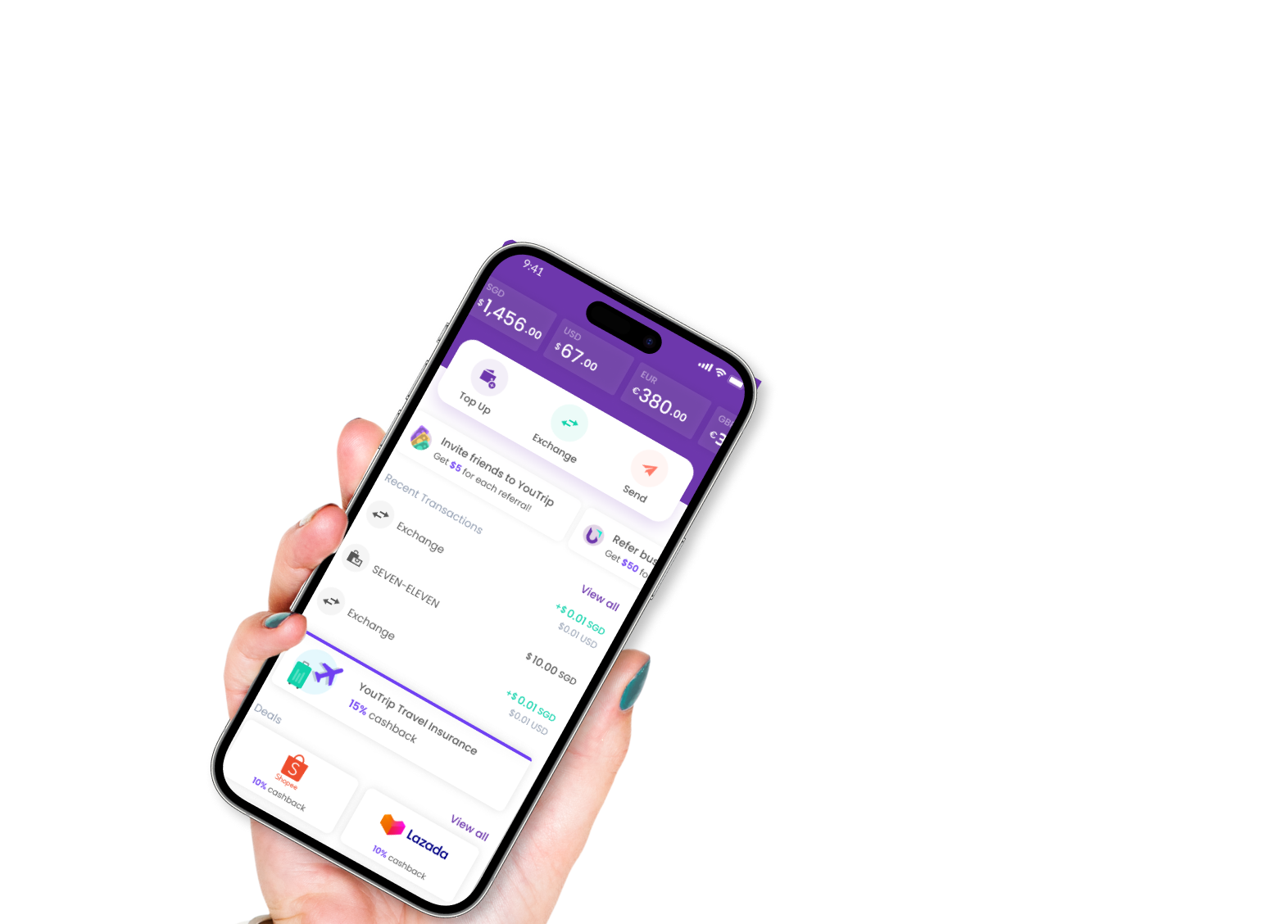

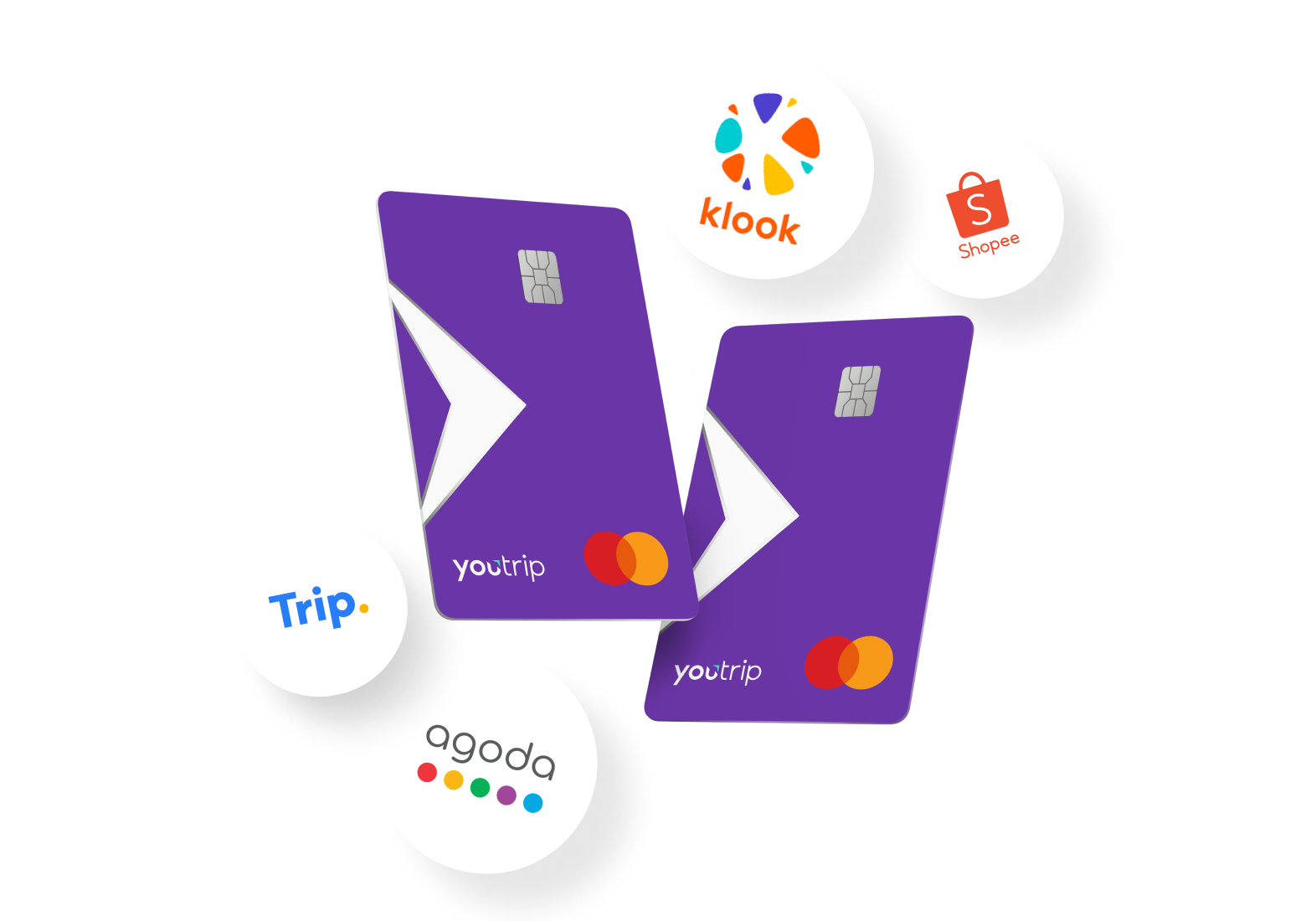

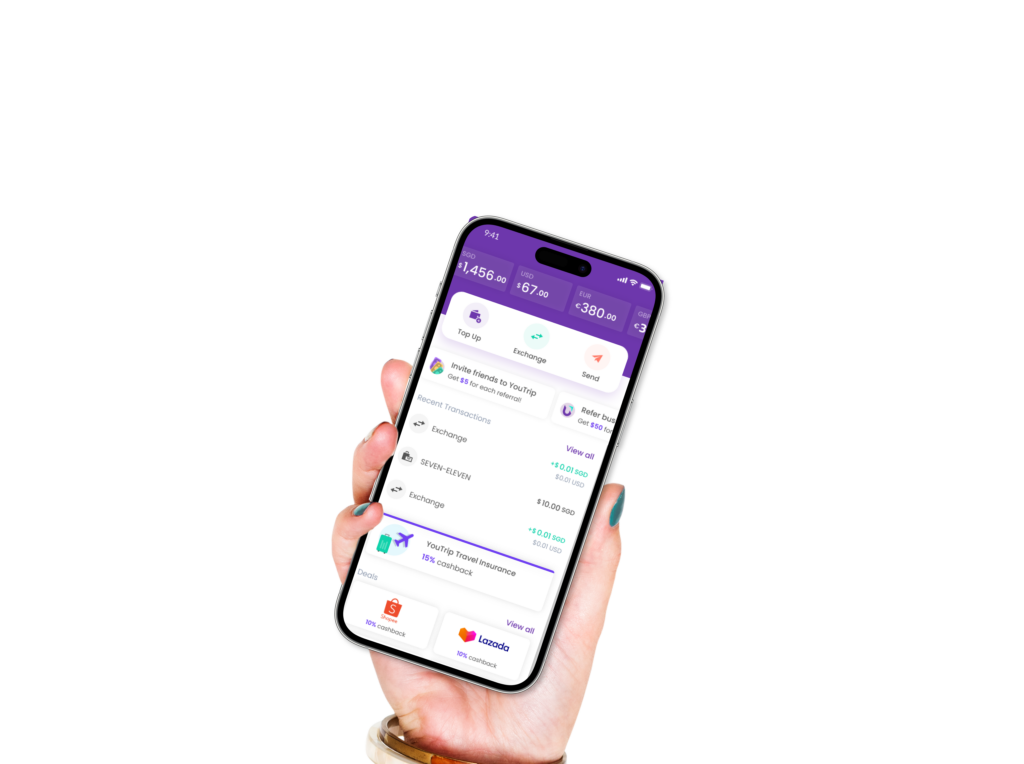

0% transaction fee anywhere! It's really simple to use to the card and you just need to top up via the mobile app. Conversion rates are better than the money changers as well.

Tay Yu Xiang

Tay Yu Xiang

YouTrip is perfect for me. I travel a lot for work. With YouTrip, I carry a lot less cash with me. It's safer and more convenient. The FX rate is extremely competitive as well.

Justin

Justin

in just 3 mins

sign up to our newsletter

need help?

best rates, it’s our thing

whenever

wherever

we got you

goodbye

hidden fees

virtually

yours

Apple Pay

& Google Pay™

on the go

can’t get safer than this

savings never

felt sweeter

you said it first

0% transaction fee anywhere! It's really simple to use to the card and you just need to top up via the mobile app. Conversion rates are better than the money changers as well.

Tay Yu Xiang

YouTrip is perfect for me. I travel a lot for work. With YouTrip, I carry a lot less cash with me. It's safer and more convenient. The FX rate is extremely competitive as well.

Justin

Fees are transparent. The card with the best rates and very convenient to use overseas.. Application is simple to use and fuss free. Great card when you go to multiple countries. Great job youtrip team! 🙂

Steve

Easy & convenient to use! You can use it worldwide even though there’s 24/7 money exchange rate on the app. Overall the best ~

Rifiqi

I get to enjoy 0% transaction fees and competitive exchange rates when I use my YouTrip Mastercard. Highly recommended.

June Liew

Easy to use, convenient for on-the-spot exchanges. Great for foreign currency on your card. great rates as well.

Alex Lim

join us for free in just 3 mins

sign up to our newsletter